This will be a post long on musing and short on evidence. But I have two anecdotes about Canadians, or at least Canadian-bound immigrants.

In grad school I met a Chinese woman who moved to Canada for her undergrad, but her express purpose was to eventually find her way into an American graduate school (which she did). She knew that not only would a Canadian undergraduate degree look good to an American Grad school, but she also knew that she could get her American visa while living as a student in Canada, and that it would be easier to do that than to get a visa while living in China. Most people don’t realize, but even if you’re accepted to a University, you aren’t guaranteed a student visa. The American state department can reject your visa if they think you’ll overstay, and the staff are very strict when issuing visas in China and India, but much more lax when issuing visas in Canada.

Now why didn’t she do her undergraduate degree in America? I don’t know, I never asked. Maybe it was too expensive, maybe she couldn’t get in. But she was open an honest that she though an American degree was better than a Canadian one, and much better than a Chinese one, and so getting an American degree was crucial for her career.

And a researcher I know at my current job has Canadian citizenship, but he and his family immigrated there with the intention of eventually reaching America. I don’t know how, but he said it’s a lot easier to get permanent residency and citizenship in Canada as opposed to America, and it’s a lot quicker. And once you’re a Canadian citizen, you have a much higher chance of getting a visa into America compared to an Indian citizen.

Like in China, the state department considers Indian citizens to be at a very high risk of overstaying their visas, and so are reluctant to give visas to them. But Canadian citizens are low risk. If you eventually want to move to America for work, moving to Canada and becoming a Canadian citizen can be a long-term strategy.

So how common is this overall? I have absolutely no idea, but I’d like to know. I know that recently both Canada and America had very high spikes of immigration. Canada under Trudeau defended its immigration policy on economic grounds as bringing in more workers to grow the economy, America under Biden instead used humanitarian grounds, as America being a beacon for the tired, poor, and huddled masses. But during this spike, there were still stories of people coming to Canada and then trying to use that to move to America.

So how true is this, and what are the implications? A troubling implication would be if Canada was seen as a “secondary” destination for many migrants, who would only go there if they thought or knew they wouldn’t be able to go to America. That would mean the international opinion of Canada’s economy is rather low, and also that it probably wasn’t receiving the best and brightest compared to America (because the best and brightest are more likely to be accepted into America).

This could also have ramifications to how Canada is affected by American policy. America is endorsing a highly restrictive immigration policy. Will this cause more immigrants to seek Canada, as they cannot reach America? Or will it cause *less* immigrants to seek Canada, as many of them *only went to Canada in order to reach America, which they now cannot do*?

Canada is also changing its policy at the same time, so teasing apart a single cause is difficult, maybe impossible. But it does make me think.

I was once talking to an econ guy at a conference, and he said that if every country on earth adopted open borders, most countries would see their immigration plummet as almost all immigrants they would have received would instead go to the United States. I don’t know if this is true, and he was an American of a certain political persuasion, so he may have had emotional reasons to believe this is true. But if anyone else out there has evidence of this, I’d love to see it.

The answer is trade-offs, Ezra Klein doesn’t contend with trade-offs. But I also wrote the title of this post to reference an old song I heard by a group called “The Klein Four,” check it out, it’s a good song if you like jokes about math and love.

I’ve discussed a lot about Ezra Klein’s abundance agenda before. To remind us, Ezra Klein says the reasons for America’s economic malaise is that we have made it impossible to build the houses, jobs, and infrastructure that we need to bring down costs and bring up wages. Housing costs will go down if we build more houses, so the government should write laws to ensure we can build more houses.

This agenda can seem very “ivory tower,” but has come into sharp focus with the creation of the bipartisan Abundance Caucus, as well as the likely next mayor of New York City coming out in support of the abundance agenda.

But the question that I want to raise is: what political group will be thrown under the bus in pursuit of abundance?

I mean this question honestly. This is not a gotcha, this is not an attack. This is my assertion that abundance *will* require trade-offs, and certain political groups *will oppose* those trade-offs no matter what. In order to enact Abundance then, you will have to choose your trade-offs, and therefore choose who goes under the bus.

Klein is not a politician, and he and his co-author have tried to assert that there really aren’t any trade-offs with abundance. We can keep *all the good things* that he and his co-partisans support without any negative side affects. And likewise the new laws we write to ensure that housing, factories, and infrastructure get built faster and more efficiently will not harm his co-partisan’s priorities whatsoever.

But I think Klein does this because he makes the classic mistake of thinking everyone has the same priorities as he does, they just don’t have the knowledge he does to realize he’s right.

So to start: will Abundance throw unions under the bus, or will it continue to allow them to have veto power over housing projects they don’t like? Josh Barro wrote about this extensively. He points out that unions in blue cities have consistently held up building projects in order to increase their own power. Unions make demands that increase the cost and time-line of a project, and if they don’t get it they use every possible veto point (such as the need to get community approval or the need to do environmental review) to prevent a project from happening.

This creates a trade-off, unions vs abundance. Klein side-steps this and tries to claim that no, there really isn’t a trade-off, and he actually wants to make it radically easier to form a union. But that isn’t important. It’s quite easy to form a union in America, it’s very difficult to exercise union power. Unions are exercising what little power they have when they hold up projects, and they do so in order to ensure the project enriches their members and not non-unionized laborers. Established unions don’t care about forming unions, they’re already established. They care about enriching their members.

So there *is* a trade-off between unions and abundance. Klein tries to handwave that somehow we remove the union veto and give them some other power and that they would accept this as a fair trade. But they simple would not. So if you remove the unions’ ability to veto infrastructure projects, then you throw the unions under the bus. If you don’t remove their veto, you walk back the abundance agenda, because you are failing to make it easier to build housing, infrastructure and jobs.

Or what about environmentalism? Energy is expensive, and it’s a huge barrier to economic growth and the abundance agenda. Right now America pays a lot less for energy than much of Europe because we allow our oil companies to frack oil out of the rocks to release it. But this is an environmental double-whammy, all that fracking harms the environment and burning all that oil accelerates global warming.

Klein’s environmental co-partisans will want to ban fracking and restrict oil, while abundance for consumers may require continued fracking so Americans can use their cars and so America’s economy can continue to use that energy. Germany and the EU have shrinking or stagnating economies in part because the price of energy there is so high.

Again Klein handwaves this by saying that we can make solar panels and solar power so cheap that energy will be cheaper that way. But this ignores present reality. Texas currently is the American leader in energy abundance, with an incredibly permissive permitting regime. It indeed leads America in the installation of solar panels. It also leads America in the fracking of oil.

If solar power were such a sure bet, then Texas energy barons would stop investing in oil and move all their money into solar panels. No company would ever willingly leave money on the table like that. But solar power *is not* a sure bet, and it still has massive difficulties that make oil viable. Battery technology is not sufficient to make solar+batteries cheaper than oil or gas for night-time power. And electric cars still aren’t cheap enough to make American switch over their ICE cars.

You can’t just “abundance” your way into ignoring economics, if you make it easy to permit *any* energy, then you will permit a lot of fossil fuel-based energy solution and piss off environmentalists. If you restrict fossil fuels, you undermine abundance by raising America’s energy prices and making it harder for Americans to drive and making it harder for American companies to operate.

I wanted to write more but I’m a bit tired and this post is very late, it should have been finished two weeks ago. But let me finish with this, every single group that supports abundance has their own group policy that they see as sacrosanct. They will support the removal of *other groups’ policies* but not their own. Abundance will therefore require finding which group is weakest, and removing their policies, or finding some compromise that pleases no one but at least gets things done.

The unions will happily undermine environmentalism and local democracy, but will never support a reduction in union power. Environmentalists will not allow environmental laws to be degraded, but may allow for a reduction in union power and local democracy. And you know what local groups think.

So when you want to build new housing or a new train line through a city, each group will block it until you make the expensive concessions necessary for their support. Abundance is all about removing those expensive concessions so it’s cheaper and easier for America to build. So the question is then clear: which group will be thrown under the bus. Until the Abundance Agenda has an answer, it will largely remain a performative slogan more than a real ideology.

Unfortunately, Klein killed my joke. Because between my last post and this one, he made his own post in the New York Times where he clarified that “Abundance” is *not* about neoliberalism. Be warned, I’m writing at night again so this post will be more streamsofconsciousness-y than the last.

First, an intro paragraph: Ezra Klein says the problem with America (and especially Blue States) is that they are Unable To Build. They can’t build rail, or houses, or energy infrastructure. And while nowhere in America can build these well, Blue States are doing *especially badly*. This inability to build means our transport is expensive, our houses are expensive, our energy bills are expensive, and we need to embrace Abundance (aka “build more stuff”) in order to fix our economy. Abundance means building lots of stuff to bring down prices and make everyone happier.

I’ve been amused to see “Abundance” described as some form of rebranded “neoliberalism.” Neoliberalism is a slippery term, but the shackling of the state was a thoroughly neoliberal project.

The above is a quote from Klein, but here he himself falls into the trap of “neoliberalism is whatever I don’t like.” No wonder neoliberalism been described as an “ideological trashbin,” neoliberalism is the political equivalent of a wastebasket taxon.

He describes this “shackling of the state” as the reason we Can’t Have Nice Things in this country, or rather it’s the reason all of our government building projects are way over-time and way over-budget. He does think that some deregulation should be done to allow the free market to build things (like houses), but he is still a partisan Democrat and believes that the government should always take the first step in transportation and energy. Secretly I also think he wants to flex his left-of-center bonafides so he can quell accusations that he’s a secret Reganite, but regardless, he says we cannot have Abundance simply by deregulating, we also have to “unshackle the state.” But what does it mean to “unshackle the state?”

See, the “shackling of the state” as he calls it was really a reaction to the post-World War 2 economic consensus. It was common consensus after World War 2 the State should be allowed to buy up land and invest in infrastructure whenever it wanted, which is exactly what Klein says they should do now, and exactly what Biden said he would do from 2020 to 2024. But the authority of the state is unchecked, it has a “monopoly on the use of force” as they say in poli-sci. So eminent domain aka *forcing people to sell their land* was the common way for the state to build infrastructure, since forced sales (rather than negotiations) are always the best way to make a project happen on-time and under-budget.

We can debate whether or not eminent domain was a bad thing, but in my experience it’s basic Democratic Party orthodoxy that it was *really really bad*. You may recall former Secretary of Transport Pete Buttigieg talking about how the highways were racist by design. This quote was wildly taken out of context, but what he meant was that the government eminent domain’d poor neighborhoods in order to build our highways. Now, in American, eminent domain still requires you to pay a “fair value” to the people whose house or land you buy up. So when using eminent domain, the government buys poor neighborhoods instead of rich ones because poor ones are cheaper to buy, this is obvious. But since minorities are more likely to be poor, this means the poor neighborhoods that were bought up and paved over to build highways were more likely to be minority ones. Hence eminent domain = bad.

In reaction to eminent domain, America “shackled the state.” The power to use eminent domain was massively curtailed, and demands were placed on the state and elected leaders to find other ways to complete infrastructure without this kind of forced-sale.

But unshackling the state is exactly what Klein wants to do to enact the “Abundance Agenda,” and that would mean allowing minority neighborhoods to be bought up and their residents displaced so the government can build infrastructure. It would also mean the government can do other things it did under the pre-shackled consensus, like flooding native tribal land to build the Hoover Dam, floodiung rural Tennessee to build the Tennessee Valley Authority dams, and in many many cases of displacing people who would rather have stayed where they were.

This unshackled state was seen as an injustice by the socially-minded on the left, and so they pushed for strong laws that would prevent the government OR ANYONE ELSE from being able to do this again. The so-called “shackling of the state” was done in the name of Social Justice, not neoliberalism.

And here is a point I would like to make: Klein routinely fails to grapple with the trade-offs that his “Abundance Agenda” would create. He says that we need to “unshackle the state” in order to build lots of good things and bring about Abundance. He says that we *used* to be a country that could do this, and points to the New Deal and the Eisenhower Interstate System as proof of this, and as a model Democrats (and America) should follow. But he doesn’t realize or fails to mention that this unshackling would cause all the problems that are still complained about to this day, bulldozed neighborhoods and displaced people.

Ezra Klein wants to build railroads in the way Eisenhower built interstates, but that’s going to mean blasting through poor neighborhoods in order to get a rail line into the city, just as Eisenhower did. That’s going to mean building across Native land because that’s the shortest way to build a line between many of our Western cities. And since minorities in America are still more likely to be poor, that means the neighborhoods you’ll be blasting through will be minority ones, and you’ll be fought every step of the way by the groups who worked to “shackled the state” in the first place.

Klein is very clearly interested in social justice, but he paints a picture in which the shackling of the state was just caused by misguided leftists and hairbrained libertarians, not his social justice co-partisans. He refuses to grapple with the question of “is it just to bulldoze a poor, black neighborhood to build infrastructure that will be used by millions?” Unless he has an answer for that, then he doesn’t actually have an answer for how to “unshackle” the state.

This refusal to grapple with trade-offs runs rampant through Klein’s Abundance Agenda. He frequently makes the claim that we just need to cut red tape and *get building* and that this will allow us to achieve our every dream. But what exactly is stopping us from building, and who demanded that red tape in the first place?

The sources of Red Tape can be discussed, but I want to keep in mind a few things:

Every source of Red Tape *agrees that we need to cut Red Tape*

Every source of Red Tape thinks that *their objectives are the most important*

Every source of Red Tape just thinks *someone else’s objectives are the ones that should be cut* in order to cut the Red Tape and achieve Abundance

Klein falls into the trap of imagining a sort of Red Tape “Legion of Doom” who just stop government projects because they’re evil and don’t like government. But in fact Red Tape is always put there at the behest of some interest group that is trying to protect its members wherever possible

The sources of red tape I’d like to discuss are, in order:

Local democracy

Environmentalism

Taxpayers

Unions

Local Democracy is the one that Klein and the Abundance folks feel the strongest in attacking. Everyone hates NIMBYs, but local democracy is more than just them. As I said in the previous post, there are usually listening sessions for any new building project to get neighbor buy-in. These sessions are a great way for NIMBYs to stop projects by demanding so many listening sessions that the project becomes too expensive to be profitable, but any other interest group can also use the demand for listening sessions in order to hamstring an unwanted project.

When framed as “NIMBYs vs infrastructure,” I’m sure it’s easy to get online consensus that local democracy should be crushed beneath the Federal boot. But your political opponents will always try to frame the argument in their way, and supporters of local democracy will frame it in terms of democracy (duh) but also minority rights (why should their minority neighborhoods and native land be forced to bear the burden of all this construction?), social justice (why are these things always built in poor neighborhoods?) and local knowledge (the DC bureaucrats need to listen to the locals because they don’t understand the needs of this area).

If you don’t have a response for these framings, then you won’t be able to bulldoze the NIMBYs and build your railroads. The problem for Klein is that this is a trade-off, are we willing to sacrifice social justice and build our railroads through a poor minority neighborhood, just like we built our highways? It’s easy to attack NIMBYs in the abstract, much harder when we have actual history telling us what happens when we *do* let the Federal Boot stamp on local democracy. And while the Interstate System is widely loved, it has seen a lot of pushback by Ezra’s ideological allies, and Ezra himself is pretending that their concerns over local democracy won’t affect his Abundance Agenda.

Next let’s discuss environmentalism, which is another soft target for the Abundance folks. Abundance folks like Klein laments that “surely we shouldn’t have years of environmental review slowing down our *wind farms*. Surely we shouldn’t allow people to block solar panels in *the dessert*”. But reframed in terms of unknown environmental risks and biodiversity and it gets a lot thornier.

The Abundance Agenda seems to argue we should be fine with building a new railroad/wind farm/solar farm without the years of environmental review demanded by environmentalists. Environmentalists will hit back that we don’t know 100% what chemicals might seep into the water lines, or how many species will go extinct due to habitat destruction, or how much deforestation and de-greening the new construction will cause. I trust the engineers to do their due diligence, and I trust the EPA to monitor situations as they come up. But can Ezra really sell that to America and the environmental movement at large?

The whole point of environmental review is preventing those kinds of “chemicals in the water/mass deforestation” catastrophes, even if the review takes years or decades (in the case of California High Speed Rail). It only takes one research paper to assert that a new train *may* lead to elevated Lithium levels in the rivers of southern California, and then you’ve lost public buy-in for the project at large. And of course if the railroad *does* lead to Lithium in the water, what then? It’s easy for Klein to talk about “cutting environmental review” but he never grapples with how to respond to the claims *within his own coalition* that doing so will make America more sick.

Abundance is an ideology that to some extent wants to be bipartisan. Klein uses Red States as his model to harangue Blue states, and congress recently created a bipartisan Abundance Caucus to champion Klein’s ideas. Although this bipartisan group still voted overwelmingly for the exact kind of anti-abundance legislation that Klein laments, so whatever. But still, I’ve used this post to discuss the conflicts between the Abundance agenda and some parts of Klein’s otherwise partisan orthodoxy, I’d like to use the next post to discuss some of its conflicts with other orthodoxies.

I’d meant these to all be one post, but couldn’t get my thoughts out in time. See you again soon.

I’ve made a few predictions over the years here, and I want to talk about two of them.

I’m declaring victory in saying that 2022 was *not* the Year Twitter Died. It was an extremely broad opinion in the left-of-center spaces that Musk was a terrible CEO, that firing so much Twitter staff would destroy the company, that it would be dead and overtaken very soon. I can concede the first one, the second two are clearly false.

The evidence from history has shown that firing most of Twitter’s staff has *not* led to mass outages, mass hacks, or the death of twitter’s infrastructure. It may seem like I’m debating a strawman, but it’s difficult to really convey the ridiculous hysteria I saw, with some claiming that Twitter would soon be dead and abandoned as newer versions of most popular browsers wouldn’t be able to access it. Likewise it was claimed that the servers would be insecure and claimed by botnets, and would thus get blocked by any sane browser protection. None of that has happened, Twitter runs just as it did in 2021. It is no less secure and it not blocked by most browsers.

Nor has the mass exodus of users really occurred. Some people think it has because they live in a bubble, but Mastodon was never going to replace Twitter and Bluesky is losing users. And regardless of your opinions on that, the numbers don’t lie.

I’ve said before that I used to be part of a community that routinely though Musk’s sky was falling. Every Tesla delay would be the moment that *finally* killed the company, every year would be when NASA *finally* kicked SpaceX to the curb, every failed Musk promise would *finally* make people stop listening to him. You’ve heard of fandoms, I was in a hatedom.

But I learned that all of that was motivated reasoning. EVs aren’t actually super easy, and that’s the reason Ford and GM utterly failed to build any. It’s not that Musk was lucky and would soon be steamrolled by the Big Boys, Musk was smart (and lucky) and the Big Boys wet their Big Boy pants and have stilled utterly failed in the EV market despite billions of dollars in free government money.

Did Musk receive free government money? Not targeted money no, any car company on earth could have benefited from the USA/California EV tax credits, it’s just that the Detroit automakers didn’t make EVs. Then they got handed targeted free money, and they still failed to make EVs.

NASA (and the ESA, and JAXA, and CNSA) haven’t managed to replicate SpaceX’s success in low-cost re-usable rockets sending thousands of satellites into orbit. So now *another* Musk property, Starlink, is the primary way that rural folk can get broadband, because Biden’s billions utterly failed to build any rural broadband.

And of course while Musk has turned most of the left against him, he has turned much of the right for him, which is generally what happens when you switch parties. And now that he’s left Trump, some of the left want to coax him back. Clearly people still listen to him even if you and I do not.

So I was very wrong 10 years ago about Elon Musk being the anti-Midas, but I learned my lesson and started stepping out of my bubble. I was right 3 years ago when I said Twitter isn’t dying, and everything I said still rings true. Big companies still use Twitter because it’s their best way to mass-blast their message to everyone in an age when TV is dying and more people block ads with their browser. The same reason people prefer Bluesky (curate your feed, never see what you don’t want to see) is the same reason Wendy’s, Barstool Sports, and Kendrick Lamar prefer Twitter. They want their message, their brand, to show up in your feed even if you don’t want to see it. It’s advertising that isn’t labeled as an ad.

So that’s what I was right about, now I’m going to write a lot *less* about what I was wrong about, because I hate being wrong.

I was wrong about how difficult it would be to get self-driving cars on all roads. In 2022 I clowned on a 2015 prediction that said self-driving cars would be on every road by 2020. Well it’s 2025, and I’ll be honest 5 years late isn’t that terrible.

At the time I thought that there was a *political-legal* barrier that would need to be overcome: how do you handle insurance of a self-driving car? No system is perfect and if there’s a defect in the LIDAR detector or just a bug in the system, a car *can* cause damage. And if it does, does Google pay the victim, or the passenger, or what? Insurance is a messy, expensive system, split into 50 different systems here in America, and I thought without some new insurance legislation (such as unifying the insurance systems or just creating more clarity regarding self-driving cars), that the companies would realize they couldn’t roll these out without massive risk and headaches.

I was wrong, I’ve now seen waymos in every city I’ve been to.

So it seems the insurance problems weren’t insurmountable, and the problem was less hard then I thought. You can read my thoughts about how hard I *thought* those problems were, but to be honest I was wrong.

A bit more streamsofconsciousness than other posts, because I’m writing late at night. But here goes:

I don’t know much about the right-of-center political shibboleths, but it’s been a shibboleth on the left that people only vote conservative because they “don’t know any better.” They’re “misinformed,” they’re “voting against their own interests,” they’re “low-information voters,” these are the only reason anyone votes for the GOP. Nevermind that the “low-information voters” tag was first (accurately) applied to the *Obama* coalition before Trump upset the political balance of power.

Remember that in the 2012 matchup, Obama voters consumed less news than Romney voters, and were less informed on the issues at large. But in those days calling someone a low-information voter was nothing less than a racist dog-whistle (at least among the left-of-center). By 2016, Trump had upended American politics by appealing to many voters of the Obama coalition, and now this racist dog-whistle was an accurate statement of fact on the left.

“Yes some voters just don’t know any better. They don’t know the facts, they don’t know right from wrong, they just don’t know. And if they don’t know, the quickest solution is to teach them, because once we give them the knowledge that “we” (the right thinking people) have, they’ll vote just like we do.”

But attacking liberals (in 2012) and conservatives (in 2016 and 2024) as “low-information” is old hat, what about attacking leftists?

That’s what the Atlantic’s Jonathan Chait has done in a recent article. Now, he doesn’t directly state “leftists are misinformed” like he would say about conservatives. It’s obvious Chait still wants leftists in his coalition and doesn’t want to insult them too badly. But he’s laying out the well-worn left-of-center narrative that his political opponents do not understand things, and that he needs to teach them how the government actually works so they can agree with his positions and support his favorite policies.

In Chait’s view, leftists just don’t get that the government is too restrictive, and that these restrictions are the cause of the housing crisis. They don’t realize it’s too regulatory, and those regulations harm growth. And they don’t get that government red tape is the reason all our infrastructure is dying and nothing new can be built. Chait attacks California High Speed Rail and Biden’s Infrastructure bill as hallmarks of this red tape. California HSR is 10 times over budget and still not a single foot of track laid down, while Biden signed the Infrastructure bill in 2021 and wrongly believed that he could have photo-ops in front of new bridges, factories, and ports in time for 2024.

The fruits of Biden’s infrastructure bills are still almost entirely unbuilt, their money still mostly unspent. And this lets Republicans make calls to overturn those bills and zero-out Biden’s spending. If his projects were actually finished on-time and during his presidency, Biden’s enemies could never attack his legacy like that. But government red tape stood in the way.

See, with claims like these, Chait is arguing in favor of the Abundance Agenda. I’m not entirely opposed to it. See mymanypostsonde-regulation.

But Chait is once again missing the mark here. He claims that Leftists don’t *understand* abundance, and that’s half of why they oppose it. He claims the other half is that they’ve built their power base as being the people who “hold government accountable” and oppose its over-reach. But Chait is mostly arguing that Leftists don’t realize that their crusade against Big Government is a “bad thing” that has made our economy worse. And I don’t think Leftists are misinformed at all, I think they just have different priorities than me and Jonathan Chait.

Let me explain though a specific example: Josh Shapiro is well-loved for repairing an I-95 overpass in rapid time. He did so by suspending all the red tape that usually slows down such infrastructure projects. Chait then argues, if we know we need to suspend the rules to get things done quickly, then why do we need to have these rules in the first place? They’re slowing us down and preventing us from building what’s needed, so shouldn’t we just remove some of them?

But here’s the red tape that Shapiro suspended:

There was no bidding process for procurement, contractors were selected quickly based on the Govenor’s office’s recommendations

There were no impact studies for the building process

On-site managers were empowered to make decisions without consulting their superiors or headquarters

Pennsylvania waived the requirement to notify locals of the construction, and to gain local approval for that construction

I don’t exactly have a problem with these ideas, and if Chait wants to make these de-regulations a central part of the Democratic brand, more power to him. But Chait is wrong that leftists are simply misinformed, I think many leftists would say that while these waivers are fine in an emergency, we should not support this deregulation for all projects, even if it saves us time and money. The reasons (for a leftist) are obvious.

Deregulating procurement is central to the Trump/DOGE agenda, and opponents say this opens the door to government graft as those in power can dole out contracts to their favorites.

Impact studies were also deregulated under Trump in two differentexecutive orders. Biden revoked both orders at the start of his term because of his focus on health and the environment. I think most leftists would assert that protecting the environment and health is more important than other government priorities.

On-site vs HQ is less of an emotive topic, but the need for “oversight” is still a driving idea any time the government Does Stuff

Waiving of financial reporting opens up accusations of fraud

Waiving environmental reviews, see point 2

Waiving local notification and buy-in. You can probably get away with this when “re-“building, but will ANY democrat stick their neck out and say locals shouldn’t have a say in new highway construction? I doubt it. Highways change communities, and any change needs community buy-in (so they say). This focus on localism is very popular on the right, left and center, no matter how much I and the Abudance-crats may oppose it.

So Chait, do the leftists not understand Abundance? Or do they have strongly-held beliefs which are incompatible with Abundance?

This whole theory of “low-information voters” is always appealing to democracies biggest losers. It’s why the GOP liked it in 2012, and it’s why Democrats like it in 2024. The idea cocoons us in a comforting lie that we alone have Truth and Knowledge, and that if only everyone was As Smart As Me, everyone would Vote Like Me.

It also seems Obviously True on the face of it. “The best argument against Democracy is a conversation with the average voter,” so the saying goes. And when you see any of your opponent’s voters interviewed directly, you can’t help but notice how much information they are *lacking*. And it’s obviously true, most people don’t know how government works, they don’t understand permitting, they don’t get that environmental impact reviews cost so much money and time. So obviously if we gave them that knowledge, they’d start voting “correctly,” right?

This misses an important point about political coalitions and humans in general: the wisdom of the crowds. Most people don’t know most things, but we all (mostly) take our cues from those who do know.

Think about the leftist coalition in America, the Berniecrats, the AOC stans, the DSA and the WFP. Most of the voters in this coalition don’t have a clue how environmental review works. But there are some in the coalition (probably including Bernie and AOC) who do know how it works, and the rest of the coalition takes its cues from those people.

There are certainly some people who have looked long and hard at the Abundance Agenda, and they have concluded that (for instance) removing environmental reviews would lead to Americans being exposed to more pollution and harmful chemicals. It was only because of environmental reviews that the EPA took action against PFAS, for instance.

So Chait is arguing that we need to reduce regulatory burden and reduce the ability of locals and activists to halt projects with their red tape and environmental reviews. I agree with this.

But Chait then argues that the only reason leftists don’t agree with us is because they don’t understand how harmful red tape and reviews are, and thus leftists have lead a wrong-headed campaign of being the people who say “no” to new buildings. I disagree with this.

I think the evidence shows that leftists simply have different beliefs than me and Chait. Leftists believe that red tape and reviews are necessary to protect the environment. And a leftist might argue that Chait complaining about environmental reviews is like a conservative complaining that “cars would be cheaper if they weren’t forced to have seatbelts and useless safety stuff.” Chait says environmental review doesn’t help us. Well I’ve never needed my seltbelt either, because I’ve never crashed.

I’m sure you can see how stupid the seatbelt argument is, well that’s probably how stupid leftists would see Chait. Yes 99% of the time an environmental review finds nothing objectionable about a project, but what about those few times when they do? Do we scrap the whole system because it’s usually a waste of time? I say again: without environmental review, the EPA would not yet have taken action on PFAS. A leftist could seriously say to Chait: do you support allowing PFAS in the water? Because it might still be allowed without environmental review.

I don’t know what Chait’s response would be, I’m sure he’d try to say “well that’s different,” because any review that *found* something was clearly a good review. But you don’t know beforehand which reviews will find something dangerous and which won’t. To a leftist, that means you have to do them all.

Now, most leftists *do not understand environmental review* just like most liberals, moderates, conservatives, and reactionaries. Most people don’t understand most things. But the leftist coalition includes people who *do* understand it, and they’ve weighed the costs and benefits and come out with a different stance than Chait has. The rest of the coalition takes its cues from the understanders, just like the every other coalition does.

But Chait’s thesis is built on a lie that because most leftists don’t understand, they’ll side with him and Abundance once they *do* understand. I disagree strongly. Most leftists will continue taking their cues from the informed leftists, and Chait is not saying anything new to inform those informed leftists. The coalition will only modify its position on this issue once the majority loses faith in the understanders (and thus seeks new ones with new positions), or when enough of the current understanders retire and are replaced by new ones. Coalitions, like science, advance one funeral at a time.

But this idea that people are misinformed and just need a smart guy like *me* to set them straight, this is a central tenant of politics that I think needs to die. You shouldn’t assume your opponents are just misinformed, you need to understand that they *actually have different ideas than you do*, and try to win them over by finding common ground. Otherwise you’ll continue to be the Loser Coalition just like Rush Limbaugh and the Romney-ites of 2012.

Answer: it’s neoliberalism. But if that answer fills you with disgust, fear, or just confusion, please read on as I promise the explanation will be worth it.

In the wake of the 2024 election, Ezra Klein and buddies published a book called “Abundance,” and in talks and interviews they have been trying to sell it as a way forward for the defeated Democrats. The key question of the book is this: if liberal policies are so great, why do blue states have the most homelessness? Why do they have the highest overruns on their infrastructure projects? Why do they have the most difficulty building renewable energy?

These are difficult questions because they cut at the heart of the liberal/progressive promise for America. There was a half-century long political touchstone (within the American media sphere) that the Democrats were who you voted for if you cared about social issues, but you voted Republican if you cared about economics. Never mind that this misses the many socially conservative/economically re-distributive voters who saw things the opposite way, this “vote Republican for the economy” belief was one that Democrats wanted to push back on.

For my entire adult life, Democrats have been making the argument that no, “Republicans are actually bad for the economy, vote Democrat if you care about economics.” In the wake of the Financial Crisis, this message resonated, but after 4 years of inflation it seems voters no longer bought it.

Worse still, Ezra Klein’s “Abundance Agenda” argues that *you can’t blame voters for coming to this conclusion*. Blue states may be the *richest states*, but it is the Red states that are *growing*. They are building housing, they are building infrastructure, and in the next census it is predicted that Blue States (California and New York especially) will lose electoral votes to Red states (such as Florida and Texas). People are literally voting with their feet, moving from Blue states to Red states when every part of the liberal mindshare says that’s insane, and that all migration should be happening in the *other direction*. The only explanation is that people believe they’ll have higher quality of life in these Red states than what they have in the Blue states, how can that be?

Ezra Klein’s answer is that Democrats haven’t lived up to their economic promise, and they need to embrace Abundance if they are going to do so.

Much of his suggestions are things I myself have blogged about, land use should be deregulated, housing and energy should be made easier to build, and the free market should at times be deferred to to bring down prices for consumers. Government bureaucrats can’t run markets.

In this sense, Ezra Klein is making a (small) break with Bidenism. Tariffs on solar panels make it more expensive to build clean energy, tariffs on lumber make it more expensive to build houses.

When it’s more expensive to build things, then the supply is lower. When the supply is lower, the price is higher. If we want consumers to enjoy low prices, we should encourage higher supply by making it less expensive to build, this is the core of the Abundance Agenda. “Build what?” you ask? Everything. Housing needs houses to be built, energy needs power plants to be built, jobs need companies and factories to be built, and the Abundance Agenda encourages policies that make it cheaper to build all those things.

See, Biden is actually a pre-Carter Democrat, recall that he was elected to the Senate in 1972. The New Deal consensus at that time included a lot of skepticism of markets, and a certain degree of autarky in which the government should step in to ensure the economy is making the things it “needs” to make. So if car companies are struggling, we need to give them subsidies or protect them with tariffs, because cars are so important. Same with solar panels, microchips, and steel.

Biden’s economic record is actually reminding me a lot of Jean Jacque Servan-Schreiber, who you may remember from previous posts. Like JJSS, Biden seemed to be trying to use government power to “direct” the economy, and my criticisms of JJSS apply just as well here: governments can’t predict the future and so don’t actually know what the best investments are. Companies can’t predict either, but at least companies have price signals and the profit motive directing them towards the best bets, governments are immune from both by their sovereign nature.

JJSS wanted the Europe of the 1960s to invest heavily in supersonic planes, but we now know that those bets were quite wasteful as the fruits of their labor (Concorde) were outcompeted by the private sector (Boeing) who had already abandoned supersonic travel entirely. Will Biden’s chip foundries built in Arizona stand the test of time? Or will they be like Concorde, an unprofitable venture held up solely by the demands of national prestige, until such time as prestige becomes to expensive to maintain?

While Ezra still sees a need for government “leadership” (which I don’t, but more on that later), he is more comfortable in the post-Carter consensus, stating that governments should cut back the regulations which prevent companies from giving us cheap goods and services. Housing is expensive because governments don’t let us build houses. Energy and infrastructure are expensive because solar farms and railroads get blocked by environmental review. Even healthcare and education are burdened by over-regulation which prevents competition and protects the current megacorporations that dominate the market.

So Ezra Klein could be most accurately described as a “left-capitalist.” He is solidly on the left with regards to all social and moral issues, but does not have the skepticism of profit and corporations that Bernie and Biden do. In other words, he’s a neoliberal.

Now that is a *very* loaded term, because my time around the Internet has shown me that many people define neoliberalism as “anything I don’t like.” But philosophically neoliberalism *was* a thing, and in many ways did represent a real ideology. It was a break with the New Deal consensus on governments directing the economy, while still accepting a government role in social welfare and poverty reduction. Carter and Clinton both governed this way, and so are usually considered “neoliberals” by people who don’t consider it a slur.

Ezra Klein is therefore arguing that this “neoliberalism” should be part of the way forward for Democrats and America at large. California and New York should take more cues from Texas and Florida, at least economically. But to do so means touching a lot of third rails within the liberal coalition:

To deregulate housing, you need to remove the ability of local residents to block new housing. This can easily be reframed as “removing local control” and “overturning democracy” if the neighborhood votes against a new house and you let it be built anyway. This deference to localism is hard to overcome politically when it’s framed in terms of gentrification and “Residents vs Corporate Developers”

To deregulate energy and infrastructure, you need to end a lot of environmental regulations. You need to get acceptance from the coalition that sometimes we’ll have to cut down a meadow to build a solar farm, or pave over a creek to build a railroad. And if there’s a species of animal or plant that *only lives* in that meadow or creek, then you have to get buy-in that biodiversity is less important that fighting climate change.

Energy and infrastructure also touch on “local control” and activist veto. Ezra Klein wants to make it easier for companies to get environmental lawsuits dismissed, and would likely applaud the recent supreme court decision on NEPA. But in any fight between “corporations” and “climate activists,” the coalition is inclined to side with the activists, and that will be hard to overcome

To deregulate schools and childcare, you need to remove laws that were put there in the name of “safety.” Many states have very low caps on child-to-adult ratio in daycares, as low as 1:3, as well regulations that the workers must have a degree in childcare and training in a wide variety of emergency medical scenarios. When a certain democrat suggested raising the child-to-adult ratio to 1:4 in one city, I saw comments that “this change will kill babies,” which is a thought-terminating incitement intended to protect regulations by force of emotion, rather than reason. If 1:4 will kill babies, then isn’t 1:3 already killing babies, since we could instead be having a 1:2 ratio? Or 1:1? At some point you have to weigh up the costs and benefits, even in cases of life and death.

And to deregulate any of these things, you need to overcome the cries that “every regulation is written in blood,” ie no deregulation should ever happen. This is yet another thought-terminating cliche but it’s one that has a lot of power on the left-side of the political spectrum.

So will Abundance succeed? Will Ezra Klein and the new “Abundance Caucus” make New York and California as affordable as Texas and Florida? Will they reverse the migration trends and made New York lose so many of its electoral votes? I don’t know, but I have more to say on this later. Now that I’ve defined what abundance is, I’d like my next post to discuss what it isn’t. Stay tuned…

Trump is an unusual figure among the world’s politicians. It is not that he is a nativist and a protectionist, but that he is open and direct about his nativist and protectionist beliefs. Trump says that foreign companies are harming American companies by undercutting on price, and that foreigners are stealing American jobs by working in America.

There are many reasons to attack these beliefs and to tell Trump he’s wrong. Here are some reasons give on the left or the right, maybe you agree with one of them:

If foreign companies sell for cheaper, than that means blocking foreign goods raises prices. And raising prices (aka inflation) directly harms all American consumers way worse than foreign goods harm a single American company

“Oh your company can’t compete? Sounds like a skill issue. Your company deserves to go bankrupt, free market in action.”

Foreigners do jobs Americans don’t want to do

It’s unethical to prevent foreigners from moving to America to look for a better life

“Oh you can’t compete against foreign workers? Sounds like a skill issue. You deserve to go bankrupt, free market in action.”

Trade barriers will wreck the economy by driving up prices, and any claims of fairness are necessarily secondary to this single overriding truth: trade barriers are bad for the economy

Politicians in and out of America have made each of these arguments in turn as they argue against Trumps new tariffs. But the single-minded opposition to tariffs hides something deeper: almost every politician globally throws up trade barriers just like Trump, but they have different excuses.

“Those goods contain chemicals that harm our health”

“Those goods contain chemicals that harm our environment”

“For national security or data privacy, we cannot allow foreigners to hold our market or buy our data”

And the old reliable: “those goods and services don’t comply with our regulations.”

This last one is pernicious because of how vapid and all-encompassing it is. It only works because people have a knee-jerk reaction against deregulation, but as I have pointed out, there’s a lot of anti-consumer regulation out there raising our prices and harming our economies. Regulation doesn’t actually mean “good,” but enough people believe it does that politicians can hide all their protectionist bullshit behind an aegis of “regulations.”

I say all this because I’m bashing the EU again today. A former EU minister of parliament put out a post which demonstrates a lot of this BS EU protectionism. I had already known that the EU uses “regulation” to protect its market from foreign goods, what is commonly termed “protectionism.” What I did not know is how much EU countries use this to protect their national markets from the single market itself.

The whole idea of the single market is free trade and free movement. If a company is allowed to sell goods in one country, it should be allowed to sell goods in all of them. If a person is allowed to work in one country, they should be allowed to work in all of them. This reduces barriers, brings countries closer together, and is much more efficient economically than a world of barriers and tariffs. It should bring everyone prosperity.

But the countries of the single market still want to “protect” their national markets and their national workers, just like Trump does. But unlike Trump, EU countries are legally forbidden from erecting tariffs. So they use health, safety, and regulation instead to do their dirty work. Here’s some examples from the article:

Denmark claiming that adding vitamins and nutrients to breakfast cereal “could be toxic,” with absolutely no justification whatsoever. The cereals are consumed EU-wide, and one would think the burden of proof would be on the accuser in that case. But no, a baseless “could be toxic” claim is enough to ban a product in Denmark unless the company making it is willing to go through a long court battle against a national government.

Spain and Italy trying to force foreign chocolate (consumed in every EU state, legally chocolate by EU law) to be explicitly marketed as “not true chocolate” even though every law says its chocolate.

France forcing Dutch biodiesel to comply with expensive testing that is waived for French biodiesel.

Germany forcing foreign professionals to undergo expensive “equivalence checks” before allowing them to work in the country. This is just more BS occupational licensing by the way, a horse-groomer shouldn’t need a license to begin with let alone an “equivalence check” to make sure their Italian license is valid in Germany.

Adding new national regulation that must be complied with *on top* of any EU regulation. This is the most pernicious, because most EU regulations explicitly mention that they are there to “harmonize” the market, make goods acceptable in every country. But EU regulations in the past decade have not decrease trade barriers, because countries have learned to add a new national regulation on top of every EU one, forcing foreign companies to increase their compliance cost if they want to break into a national market.

For years and years, Europe was indeed a continent of decreasing trade barriers. While they continued to be strongly protectionist against the outside world (erecting anti-GMO laws primarily as protectionism for EU farms), they were at least reducing barriers within the block. But Europe is not immune to the anti-globalization sentiment that has swept across Britain and America since 2016. It’s just that much like Biden, European politicians are caught between maintaining their appearance as internationalists while still wanting to be protectionists and nativists.

So rather than erect tariffs, the EU countries have recently relied on “soft” barriers, barriers which don’t *technically* forbid entry of foreign goods, but which do place onerous costs on anyone who wants to enter the market. And a supposed internationalist has to justify their protectionism somehow, they don’t have Trump’s luxury of just honestly stating their beliefs. So they rely on their old faithful excuses: health and safety.

Biden claimed that foreign goods were a national security issue. China was the security threat that we were supposedly countering, but we countered China in part by banning Vietnamese solar panels, Mexican cars, and Canadian lumber.

And for the EU countries health, environmentalism, and data privacy are paramount. They’re part of what separates Europe from America after all. So who cares that added calcium isn’t unhealthy, or that Dutch companies are making biodiesel the same way French companies do, if it’s foreign we can claim it’s unhealthy and unsafe by default. And then we ban it until they comply with our expensive tests, or until they start making the product in our country, or until they stop being foreign and sell themselves to locals.

This is exactly what Biden and Trump wanted: American goods instead of foreign goods. But the EU countries use regulation to achieve this goal since they can’t tariff the single market.

And this is one of the main reasons I push back against regulation. I’ve said over and over, regulation is not intrinsically good or bad. Good regulation is good, bad regulation is bad. But I’ve seen over and over how politicians hide their protectionism behind a coat of regulation. And I’ve seen how most people have an intrinsic distrust of deregulation, meaning whenever I point this protectionism out I’m accused of wanting to destroy health and safety.

“Foreign cereal is unhealthy,” “foreign biodiesel is bad for the environment,” “foreign Tech companies will steal our data,” it’s very easy to just claim this without evidence and get people on board with you. And it’s *surprisingly* easy to do when “foreign” just means another country in the EU, wasn’t Europe supposed to have solidarity?

And it’s impossible to prove a negative, so proving that the cereal is no less unhealthy, the biodiesel is no different, the foreign Tech has the same policies as the native Tech, this is a losing proposition and expensive to boot. So protectionism goes on unabated, and then people wonder why the EU is still falling behind economically. Well Mario Draghi told you why, it’s because even before Trump the EU was putting tariffs on itself.

I write this in part out of frustration and in part as an attempt at education. People are negatively polarized against Trump, and so even people who never heard or cared about tariffs are deciding that tariffs are bad and we shouldn’t do them. Some neoliberal Democrats are hoping that this lets them finally remake the coalition, and kick out the protectionists like Biden and Sanders in favor of rebuilding the Clinton-Bush-Obama consensus of free trade.

But even if this happens, I’ve seen way too much evidence that this will not be a radical remaking of ideology. Protectionism will, as it has in the EU, simply become the purvey of health and safety. Even the neoliberals of the party have trouble arguing against health and safety, especially when Democrats as a whole are so negatively polarized against deregulation.

So that’s what I really wanted to say: regulations are not always good. They are not always bad, but they are not always good. Don’t assume that just because the government banned something, it was right to do so. Be open to the possibility that they’re protecting their markets just like Trump is.

Note that this one’s more rambly than I wish, but I have a lot of thoughts and am not good at editing. Suggestions for how to cut this down are appreciated if you want to leave a comment or an email.

You might as well be lighting your money on fire…

When talking about the American vs European economies, the discussion always turns towards Tech. “Europe missed the Tech boom” is a true, but surface level description of Europe’s stagnation in high tech industries. Cloud computing, social media, AI, all the buzzwords of the last 20 years have been American, and some wonder why Europe doesn’t have trillion-dollar companies like Apple and Microsoft. I’ve already pushed back on the “cultural” explanations for this, but I want to look deeper at some of the proposed solutions for helping Europe’s economy catch up.

If you ask why Europe has a smaller Tech industry, there’s a few common answers given. One is that Europe is fragmented linguistically, most people don’t speak each other’s language, while America has 300 million people all speaking one language. But I’ve never been convinced by the argument that tech companies stop at the border.

You can maybe make the argument that social media spreads fastest among people who speak the same language, but I’ve never seen this argument be well-quantified. Facebook is used by half the earth’s population, they don’t all speak English, so why did it spread so easily even after maxing out in the English-speaking world? And TikTok has been a viral hit among westerners, even though it started in China. The language argument is often presented as obvious but without any evidence to support it, and I don’t think it’s reasonable until I see some evidence.

Furthermore, social media is just a tiny piece of the Tech industry. Apple, Microsoft, Spotify, Samsung, these aren’t social media companies. So what explains why half of them are American, and the non-American ones aren’t even in the top 10?

Another argument is that Europe is fragmented economically. Still, I don’t really buy this. It’s true that Europe is not wholly unified, different countries have different regulations. But the EU is a common market of goods and services, overwhelmingly products sold in one country can likewise be sold in another. If there was a European version of Apple or Samsung, their smartphones would almost certainly be buyable in any EU country. Indeed, the market fragmentation never stopped Nokia from its 1-time dominance of cell phones, so why did this fragmentation prevent the emergence of a European smartphone company, if it never stopped the top European cell phone company?

The final common answer is the one I want to discuss today: European investment is low because there is no unified capital market. German investors invest in German companies, French investors in French companies, and this drastically limits how much capital is available for startups. While Europe is trying to have 27 different capital markets, American capital is clustered in just 1 (Silicon Valley) or 2 (if you count Boston, New York, or one of the other “also rans”).

I buy this argument more, but I want to start with some clarity on what it *really means* for a capital market to be “unified.”

We’d say a market is unified when investors from one area are equally capable of investing in any other area. Why might investors not invest across the border? Tax and regulation mostly.

Taxes don’t have to be *higher* to deter investment, *different* is more than enough. Think of capital gains tax when an investor sells something they’ve invested in. Some places allow a lower tax when you hold the investment longer (long-term capital gains), while others don’t make a distinction. This may lead to a lower tax burden overall, but more tax-season headache in proving how long each investment was held, and proving it was held in the correct jurisdiction which allows this long-term capital gains distinction. Sometimes it’s better to just invest everything in one place and hire less accountants.

Different regulations would also be self-explanatory, there’s more bureaucratic overhead in understanding and applying different regulations for each different investment. But here we come to the difficult part, and why I think Draghi’s drive for unification will face stiff headwinds. Regulations have a moral component for lack of a better word. When discussing regulations online, it’s not uncommon to see “regulations are written in blood” as an emotive argument put forth against deregulation. Any attempt to pair back anything in the way of “red tape” faces a mountain of pushback from voters, and unifying the regulations will require *some* deregulation.

*Some* country’s regulations will have to be cut, even if they’re simply replaced with those of another countries. Even if regulations are “harmonized” by trying to bring them closer together, that still means some things get cut and some things get added. And this will necessarily inflame the passions of the voters and commentators who say that “regulations are written in blood.” Because while regulation of the capital markets might not have to do with healthcare and worker’s rights directly, they do have much to do with bankruptcy and ownership, which can be even more emotive.

Trump is often jeered for his numerous corporate bankruptcies. He in turn calls bankruptcy a smart business move when needed. It’s true that an investor can expect 9 investments to go bust for every 1 that succeeds. And it’s true that American bankruptcy laws are quite lenient. And it’s also true that a smart investor be foolish to not take advantage of any edge the law can give them, lenient bankruptcy is one such edge.

But bankruptcy stirs passions because someone’s left holding the bag. If Europe is going to unify its capital markets, it’s going to inflame those passions. When the banks went bankrupt in 2008, it stirred immense passion because of who had to pay and who was left holding the bag. Changing these laws raises the specter of the financial crisis, and any recent bankruptcies will get put under a microscope to point out how things would be different in a unified EU capital market.

To put some meat on these bones, let’s say a car company is going bankrupt in Bulgaria. We’ll call it “Bulgarian Cars,” its owner and CEO is Mr Car, its workers belong to the “United Car Workers Union,” UCWU. It has purchasing agreements for steel with “Steely Corp” and its sole creditor is “Big Banking,” who is unfortunately unaware that Mr Car is about to go bankrupt.

Under the current Bulgarian system, Big Banking can (if they desire) simply take possession of all the “Bulgarian Cars” assets, and sell them in a fire sale to get back the money they are owed. This means the factory, the showroom, and anything else could be closed down in an instant. Big Banking gets back their money, Mr Car is broke, UCWU are out of their jobs, and Steely Corp lost its biggest customer.

But how would this situation be effected by Draghi’s directive to unify EU capital markets? How would the bankruptcy be altered? Who would win, and who would lose?

Draghi has already signaled that unified EU bankruptcy must allow for “debtor in possession,” meaning Mr Car can keep control of his company while working out a repayment plan with Big Banking. This system allows Mr Car (or any investor) to try to rescue their company, even in bankruptcy. It’s part of what made Trump’s bankruptcies so painless.

In France, a debtor is immediately granted relief from creditors upon filing restructuring plans. In Germany, the debtor may *request relief*, but it isn’t automatic. But if the capital markets are to be unified, Bulgaria must follow the direction of France and Germany and give Mr Car a reprieve from his creditors.

But should Mr Car even be *granted* relief? He drove the company into the ground in the first place! Why does he get to stay in charge, paying himself an obscene salary all the while? Draghi’s unified capital markets would allow a lot more “Trump-like” bankruptcies ripe for this kind of outrage-bait, with a villainous CEO stiffing creditors, unions, and business partners while still bringing home fat checks.

And what happens to UCWU? They just finished negotiating a new contract with Bulgarian Cars. The contract included conditions and a long notice period before a new contract can be renegotiated. But most EU countries allow the suspension of a union contract to help the company exit bankruptcy. So Draghi’s unified capital market raises the possibility of workers losing out so that bankers and executives can keep the company going. Workers’ pain for bosses’ gain.

And through all this, what about Steely Corp, who just lost its biggest customer? Bankruptcies are always politically fraught as they can cause a domino effect into other industries. This is why some nations focus so much on business continuity, even if it comes at the expense of creditors and workers. Steely Corp will want to lobby the government that UCWU and Big Banking can go to hell, they want to ensure that Bulgarian Cars returns to solvency no matter what. Otherwise Steely Corp itself may go under, and the national news will blame the Government for letting not one, but *two* major employers go bankrupt.

How much will Draghi’s unified capital market allow Governments to “save” companies this way? Under certain restructuring scenarios, the Government will essentially be picking winners and losers in the market. Demand Big Banking take a debt restructuring, demand UCWU accept a new contract, and you’re making banks and workers lose so that car and steel companies can win. This doesn’t always fly with EU rules around fairness, and certainly won’t fly with some sections of the commentariat.

This post was a lot less focused than usual, but it’s been in my mind for weeks. “Unify the EU’s capital markets” sounds so obvious, why haven’t they done it? They haven’t done it because it involves politically fraught trade-offs about ownership and hierarchy. “Who wins and loses in a bankruptcy case” is just the top of the mountain. Questions of equity investment, investor’s rights, corporate governance, union rights, these are also fraught questions that will have to be answered in a unified capital market. Whatever answer is chosen will inevitably piss *someone* off, which is why countries are so slow to change these laws. But until countries are willing to make big changes, the EU capital markets will never be unified.

Whenever you’re forecasting future trends, there are two general rules for the hack forecaster:

1. Every good trend will continue forever

2. Every bad trend will turn around soon

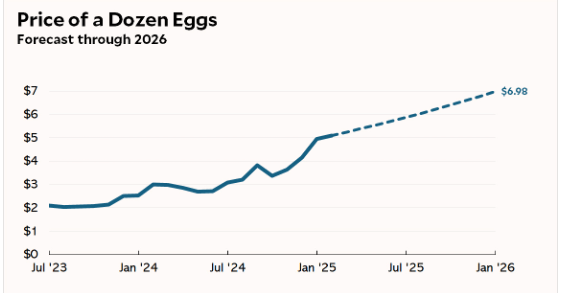

This doubly true when your forecasting has a political purpose, in which “good” and “bad” can be thought of as “supports” and “doesn’t support” your chosen narrative. A certain twitterati demonstrated this succinctly in their egg prices prediction from earlier this year:

Now I don’t want to dunk too hard on this prediction (the man died between when I first saw this and when I finally got around to posting about it), but it seems like the clearest cut case of motivated reasoning I can find. The writer was a political blogger who didn’t like the current US administration. Saddling the administration with ever-rising prices sends a strong signal that “this administration is bad for the economy.” So that was the prediction they wanted, and that was what they ran with.

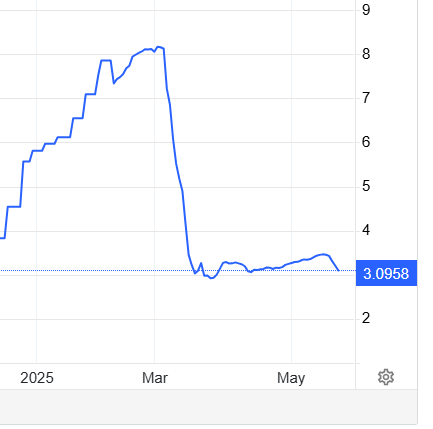

Unfortunately for motivated reasoning, this is the chart of US egg prices since the start of the year.

Source, that 3.0958 just rounds to $3.10 by the way

Trends don’t usually continue monotonically forever.

Why does this matter? Well it doesn’t matter much, this is a small post. But I wanted to make clear that forecasting is easy to do when you don’t expect accountability. It’s the easiest thing in the world to draw a trendline continuing forever to support your narrative, and if you ever get pushback later for being wrong you can attack the complainers for “focusing on the past.”

I think there needs to be a lot more social accountability in forecasting. We need to stop giving a microphone to people who constantly proclaim a doom or paradise that never comes. And our society needs to be willing to hold people accountable for their predictions.

Back when 538 still existed and was run by Nate Silver, the thing that impressed me most about their predictions was the honesty with which they *scored* those predictions after-the-fact. Every election cycle they looked at every race for which they made a prediction and compared the predictions to the actual outcomes.

And surprise surprise, predictions from an actual data scientist were quite accurate. People hate on Nate Silver for predicting Trump had a 30% chance of winning in 2016 (instead of 100%, since he *did* win, or 0% since so many people claimed he could *never* win). But true to form, any event that 538 gave a 30% chance to had about a 30% chance of happening. Over the hundreds of elections that they predicted, they gave out a lot of 30% chances, and yes those 30% events did happen 30% of the time. They didn’t *always* happen, they didn’t *never* happen, they happened about 30% of the time.

That’s the kind of accountability we need, and its a shame that we lost it along with 538.

Glacier National Part in Montana [has] fewer than 30 glaciers remaining, [it] will be entirely free of perennial ice by 2030, prompting speculation that the park will have to change its name – The Ravaging Tide, Mike Tidwell

Americans should plan on the 2004 hurricane season, with its four super-hurricanes (catagory 4 or stronger) becoming the norm […] we should not be surprised if as many as a quarter of the hurricane seasons have five super-hurricanes – Hell and High Water, Joseph Romm

Two points of order:

In 2006, when Mike Tidwell wrote about glaciers, Glacier national park had 27 glaciers. It now has 26 glaciers, and isn’t expected to suddenly suddenly lose them all in 5 years.

Since 2007, when Joseph Romm wrote about hurricanes, just four hurricane seasons have had four so-called “super-hurricanes,” and just one season has had five. The 2004 season has not become the norm, and we are averaging less than 6% of seasons having five super-hurricanes

I do not write this to dunk on climate science, I write only to dunk on the popular press. The science of global warming is fact, it is not a myth or fake news. But the popular press has routinely misused and abused the science, taking extreme predictions as certainties and downplaying the confidence interval.

What do I mean by that? Think of a roulette wheel, where a ball spins on a wheel and you place a bet as to where it will land. If you place a bet, what is the maximum amount of money you can win (aka the “maximum return”)? In a standard game the maximum amount you can win is 36 times what you bid, should you pick the exact number the ball lands on. But remember that in casinos, the House Always Wins. Your *expected* return is just 95/100 of your bid. You’re more likely to lose than to win, and the many many loses wipe out your unlikely gains, if you play the game over and over.

So how should we describe the statistical possibilities of betting on a roulette wheel? We should give the expected return (which is like a mean value how much money you might win), we should give the *most likely* return (the mode), and we should give the minimum and maximum returns, as well as their likelihood of happening. So if you bet 1$ on a roulette wheel:

Your expected return is 0.95$

Your most likely return is 0$ (more than half of the time you win nothing, even if betting on red or black. If you bet on numbers, you win nothing even more often).

Your minimum return is 0$ (at least you can’t owe more money than you bet), this happens just over half the time if you bet on red/black, and happens more often if you bet on numbers

Your maximum return is 36$. This happens 1/38 times, or about 2.6% of the time.

But would I be lying to you if I said “hey, you *could* win 36$”?

By some standards no, this isn’t lying. But most people would acknowledge the hiding of information as a lie of omission. If someone tried to entice someone else to play roulette only by telling them that they could win 36$ for every 1$ they put down, I would definitely consider that lying.

So too does the popular press lie. Climate science is a science of statistics and of predictions. Like Nate Silver’s election forecasting, climate modeling doesn’t just tell you a single forecast, they tell you what range of possibilities you should expect and how often you should expect them. For instance, Nate Silver made a point in 2024 that while his forecast showed Harris and Trump with about even odds to win, you shouldn’t have expected them to split the swing states evenly and have the election come down to the wire. The most common result (the mode) was for either candidate to win *all* the swing states together, which is indeed what happened.

Bad statistics and prediction modellers will misstate the range of possible probabilities. They will heavily overstate their certainties, understate the variance, and pretend that some singular outcome is so likely as to be guaranteed.

This kind of bad statistics was central to Sam Wong of the Princeton Election Consortium‘s 2016 prediction, which gave Hillary Clinton a greater than 99% chance of victory. Sam *massively* overstated the election’s certainty, and frequently attacked anyone who dared to caution that Clinton wasn’t guaranteed to win.

Nate Silver meanwhile was widely criticized for giving Hillary such a *low* chance of victory, at around 70%. He was “buying into GOP propaganda” so Sam said. Then after the election Silver was attacked by others for giving Clinton such a *high* chance, since by that point we knew she had lost. But 30% chance events happen 30% of the time. Nate has routinely been more right than anyone else in forecasting elections.

I don’t doubt that some people read and believed Sam Wong’s predictions, and even believed (wrongly) that he was the best in the business. When he was proven utterly, completely wrong, how many of his readers decided forecasting would never be accurate again? How much damage did Sam Wong do to the popular credibility of election modeling?

However much damage Sam did, the popular press has done even more to damage the statistical credibility of science, and here we return to climate change. Climate change is happening and will continue to accelerate for the foreseeable future until drastic measures are taken. But how much the earth will warm, and what effects this will have, have to be modeled in detail and there are large statistical uncertainties, much like Silver’s prediction of the 2016 election.

Yet I have been angry for the last 20 years as the popular press continues to pretend long-shot possibilities are dead certainties, and to understate the range of possibilities. Most of the popular press follows the Sam Wong school.

In the roulette table, you might win 36$, but that’s a long-shot possibility. And in 2006 and 2007, we might have predicted that all the glaciers would melt and super-hurricanes would become common. But those were always long-shot possibilities, and indeed these possibilities *have not happened*.

The climate has been changing, the earth has been warming, but you don’t have to go back far to see people making predictions so horrendously inaccurate that they destroy the trust of the entire field. If I told you that you were dead certain to win 36$ when putting 1$ on the roulette wheel, you might never trust me again after you learned how wrong I was. Is it any wonder so many people aren’t trusting the science these days, when this is how it’s presented? When we were told 20 years ago that all the glacier in America would have melted by now? Or that every hurricane season would be as bad as 2004?

And it isn’t hard either to find numerous even more dire predictions couched in weasel words like “may” and “possibly.” The oceans “may” rise by a foot, such and such city “may” be under water. It’s insidious, because while it isn’t *technically* wrong (“I only said may!”) it makes a long-shot possibility seem far more likely than it really is. Again, it’s a clear lie of omission, and it’s absolutely everywhere in the popular press.

We have to be accurate when modelling our uncertainty. We have to discuss the *full range of possibilities*, not just the possibility we *want* to use for fear-mongering. And we have to accurately state the likelihoods for our possibilities, not just declare the long-shot to be a certainty.